")

Back to Journals » ClinicoEconomics and Outcomes Research » Volume 17

Time-Driven Activity-Based Costing for Cervical Myelopathy Surgery: A Step Towards Total Episode Costs

Authors Keppetipola KM, Leibold A, Trivedi J, Kabani AS , Sarikonda A, Self DM, Isch EL , Glener S, Prasad S, Jallo J, Heller JE, Harrop J, Vaccaro AR, Sivaganesan A

Received 8 January 2025

Accepted for publication 21 March 2025

Published 3 June 2025 Volume 2025:17 Pages 419—428

DOI https://doi.org/10.2147/CEOR.S502217

Checked for plagiarism Yes

Review by Single anonymous peer review

Peer reviewer comments 3

Editor who approved publication: Dr Samer Hamidi

Kavantissa M Keppetipola,1 Adam Leibold,1 Jay Trivedi,1 Ashmal Sami Kabani,1 Advith Sarikonda,1 D Mitchell Self,1 Emily L Isch,2 Steven Glener,1 Srinivas Prasad,1 Jack Jallo,1 Joshua E Heller,1 James Harrop,1 Alexander R Vaccaro,3 Ahilan Sivaganesan4

1Department of Neurosurgery, Thomas Jefferson University and Jefferson Hospital for Neuroscience, Philadelphia, PA, USA; 2Department of General Surgery, Thomas Jefferson University, Philadelphia, PA, USA; 3Rothman Orthopedic Institute, Philadelphia, PA, USA; 4Department of Spine Surgery, Hospital for Special Surgery, Naples Comprehensive Health, Naples, FL, USA

Correspondence: D Mitchell Self, Department of Neurosurgery, Thomas Jefferson University, 909 Walnut Street, Philadelphia, PA, 19107, USA, Email [email protected]

Introduction: Time-driven activity-based costing (TDABC) is a highly accurate method for determining the true cost of delivering a healthcare service. However, TDABC is most often applied to a singular phase of care such as an outpatient visit or a surgical event. Here we broaden the scope by using TDABC to estimate the costs of surgically treating cervical myelopathy – from the moment of surgical scheduling until post-operative hospital discharge.

Methods: In a single-center retrospective study at a large tertiary academic institution, TDABC was employed to measure pre-operative, intra-operative, and post-operative (inpatient) costs for 63 patients undergoing elective surgery for cervical myelopathy. Cost patterns among different surgical approaches (anterior, posterior, anterior/posterior) were analyzed using generalized linear models and the Kruskal–Wallis test.

Results: 63 consecutive patients who underwent elective surgery for cervical myelopathy were examined (anterior approach: 36.5%, n=23; posterior approach: 54.0%, n=34; anterior/posterior approach: 9.5%, n=6). The average pre-operative, intraoperative, and postoperative costs were $352.83 ± $205, $10,809.09 ± $6052.69, and $5327.07 ± $5114.78, respectively. The average total episode cost for all cases was $16,488.99 ± $8,181,777. Kruskal–Wallis analysis revealed that total episode cost for the anterior-posterior approach was significantly higher than for both the anterior (p< 0.001) and posterior approaches (p< 0.05), while the total episode cost for the anterior approach was significantly less than that of the posterior (p< 0.001).

Conclusion: We have demonstrated the feasibility of TDABC for estimating a large fraction of total episode costs for the surgical treatment of cervical myelopathy. This may also be the first attempt at understanding episode costs across multiple surgical options for a given spinal diagnosis, which will be relevant as condition-based bundled payments emerge. As expected, anterior cervical surgeries incurred lower costs than posterior surgeries, which incurred lower costs than anterior-posterior surgeries.

Keywords: time-driven activity-based costing, spine surgery, health economics

Introduction

Healthcare costs in the United States have become unsustainable.1 One driver of this crisis appears to be the “fee-for-service” reimbursement model, wherein providers are paid for the volume and complexity of their care, rather than the outcomes of their care. In response, there has been a shift towards “value-based reimbursement”, where value is defined as the outcomes achieved per dollar spent.2 Examples include the Bundled Payments for Care Improvement (BPCI) program, administered by the Centers for Medicare and Medicaid (CMS), and various episode-based payment models based on direct-to-employer contracts.3,4

Inherent in these value-based reimbursement models is an assumption of some financial risk by providers.5 If the costs of executing a surgical episode exceed the pre-determined payment, providers stand to lose money. It is therefore incumbent upon providers to understand the true costs of their care, and time-driven activity-based costing (TDABC) is a highly accurate (but rarely used) methodology for doing so.6 TDABC uses process maps to identify every personnel and material resource involved in a phase of care, assigns a per-minute cost to each resource, and then multiplies these costs by the time spent with a patient to create a total estimate. We have previously demonstrated the utility of TDABC for the operative phase of spine surgery,7–10 but for the methodology to be truly useful, it must be expanded to capture a greater fraction of total episode costs.

Recent projections based on analysis of the National Inpatient Sample indicate that the annual volumes of cervical spine surgeries are expected to rise substantially over the next two decades. Specifically, the annual number of anterior cervical discectomy and fusion (ACDF) procedures is projected to increase by 13.3%, from approximately 153,288 cases in 2020 to 173,699 cases in 2040. In parallel, posterior cervical decompression and fusion (PCDF) volumes are anticipated to grow by 19.3%, rising from about 29,620 procedures in 2020 to 35,335 procedures in 2040. When stratified by age, the largest absolute increases in ACDF are expected in the 45–54 and 75–84 age groups, whereas for PCDF, the most pronounced increase is projected in the 75–84 cohort—with additional notable proportional growth in patients aged ≥85 years. These trends underscore a rising demand for cervical spine surgeries in an aging population, thereby justifying the need for our comprehensive cost analysis using time-driven activity-based costing (TDABC) to better inform resource allocation and value-based reimbursement models.11

In this study, we use TDABC to estimate the costs of surgically treating cervical myelopathy – from the moment of surgical scheduling until post-operative hospital discharge. We included patients undergoing different procedures for the same diagnosis, so as to compare episode costs and create a foundation for condition-based bundled payments.

Methods

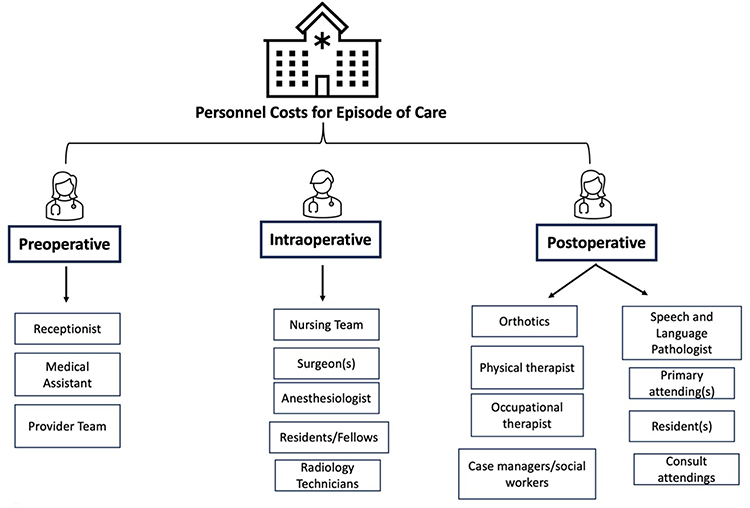

This is a retrospective study of all neurosurgical patients who underwent elective surgery for cervical myelopathy from June 2022 to October 2022 at a large, tertiary academic institution. This study was approved by the Thomas Jefferson University Institutional Review Board under a universal Quality Improvement protocol. Informed consent was deemed unnecessary for this study; however, all procedures adhered to the ethical guidelines outlined in the Declaration of Helsinki. Our Institutional Review Board (IRB) approved a waiver of informed consent for this study, as it involved retrospective data analysis without direct interaction with patients and presented minimal risk to participants. Three distinct phases of care were analyzed: the pre-operative outpatient visit, the surgery itself, and the post-operative inpatient stay. Process maps were created for each phase, establishing the various personnel and material resources involved. Only personnel costs were captured for the pre- and postoperative periods, while both direct (supply and personnel) and indirect costs were calculated for the intraoperative period, as detailed in previous studies.7–10 Our strategy for calculating personnel costs is visually represented in Figure 1. Patients were excluded from the study if they did not have reliable timestamps present in the EMR.

|

Figure 1 Strategy for Personnel Cost Calculations. |

We tracked the following personnel in the pre-operative phase: office receptionist, medical assistant, clinic nurse, neurosurgery resident/fellow, and the attending surgeon. In the post-operative phase, we tracked the following personnel: orthotists, physical therapists (PT), occupational therapists (OT), case managers/social workers (CM/SW), speech and language pathologists (SLP), residents, consult attendings, and primary surgical attendings. The cost per minute for each professional was estimated using market averages for compensation as listed on major online recruitment websites. Annual salaries for each personnel type were then used to back-calculate cost-per-minute, which was then multiplied by the minutes spent with the patient. This comprised total personnel cost.

Time spent with patients was estimated using two methodologies. First, if available, timestamp data for each personnel type was extracted from the EMR. If this data was not available, then time estimates were derived by observing general clinical workflows and querying the relevant personnel. As mentioned previously, supply costs were captured for the intra-operative phase but not for the pre-operative and post-operative phases. Intraoperative costs, which are divided into direct and indirect costs, were calculated using our previously published TDABC methodology.7–10 This method captures every personnel and material resource involved in the operating room, from the radiation technicians and the custodial staff to the pharmaceuticals and consumables.

Statistical analysis was performed using RStudio 2023.06.0. Means ± standard deviations and medians (IQR) were calculated for each sub-component of cost and total cost, and they were then stratified based on surgery type (anterior, posterior, or anterior/posterior) as well as number of levels fused. A generalized linear model (GLM) was constructed to compare the costs of different surgery types, while adjusting for potential confounders (age, sex, race, payor, surgeon, and location). Homogeneity of variances and normality tests were run to check the best fit for regression model. Since our data did not follow a normal distribution, a Kruskal–Wallis (KW) rank sum test was performed to compare costs between surgery types.

Results

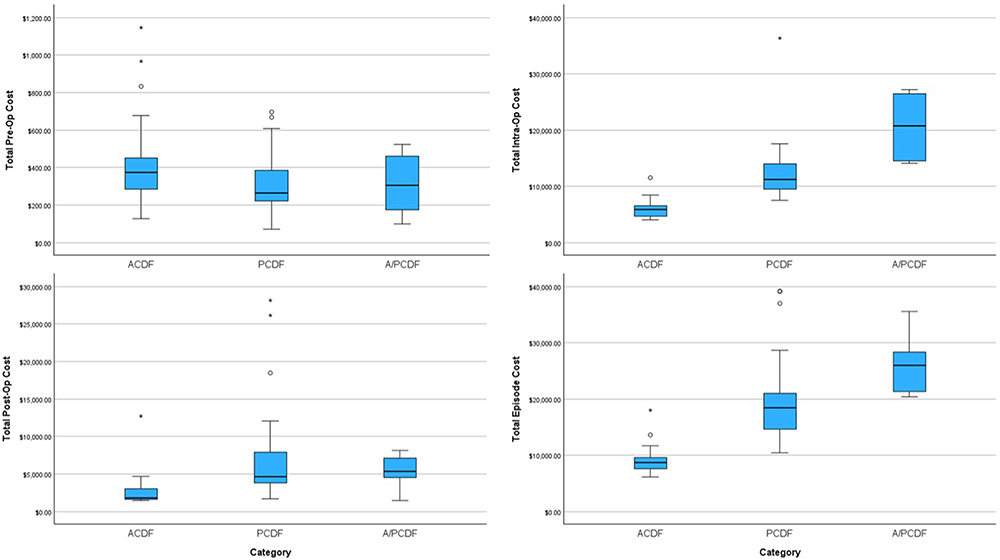

63 consecutive patients who underwent elective surgery for cervical myelopathy were included in this retrospective study period (anterior approach: 36.5%, n=23; posterior approach: 54.0%, n=34; anterior/posterior approach: 9.5%, n=6). Baseline characteristics of our study population are shown in Table 1. The average pre-operative cost was $352.83 ± $205.68 (anterior: $424.34 ± $254.13; posterior: $311.63 ± $162.84; anterior/posterior: $312.17 ± $168.33). The average intra-operative cost was $10,809.09 ± $6052.69 (anterior: $5950.66 ± $1693.03; posterior: $12,361.47 ± $5030.44; anterior/posterior: $20,636.28 ± $5818.06). The average post-operative cost was $5327.07 ± $5114.78 (anterior: $2858.75 ± $2361.31; posterior: $6995.64 ± $6125.13; anterior/posterior: $5333.68 ± $2300.05). The average total episode cost was $16,488.99 ± $8,181,77 (anterior: $9233.75 ± $2579.16; posterior: $19,688.74 ± $7211.29; anterior/posterior: $26,282.13 ± $5622.19). A breakdown of personnel costs by procedural modality is shown in Table 2.

|

Table 1 Baseline Characteristics |

|

Table 2 Generalized Linear Regression Models |

Specific details regarding the average cost for each personnel type for all three stages of care (preoperative, intraoperative, and postoperative) are shown in the Appendix Tables 1 and 2.

In a generalized linear regression model (GLM) adjusted for age, sex, race, payor, surgeon, and location, there was no significant association between surgery type and pre-operative personnel costs. Adjusted regression analysis did reveal that the posterior and anterior-posterior approaches were associated higher intra-operative costs as compared to the anterior approach ($7671.61, p<0.001 for posterior; $15,107.02, p<0.001 for anterior-posterior). Furthermore, adjusted regression analysis showed no association between surgery type and post-operative personnel costs. Finally, the posterior and anterior-posterior approaches were associated with higher total cost as compared to the anterior approach ($9594.73, p<0.001 for posterior; $17,470.83, p<0.001 for anterior-posterior). These results are summarized in Table 3.

|

Table 3 Mean Difference of Cost Between Each Procedural Category |

Given that our data did not follow a normal distribution, rank sum post-hoc analyses were conducted using the non-parametric KW test. There was no significant difference between the surgery types for pre-operative costs. The intra-operative cost of the anterior approach was significantly less than that of the posterior approach (mean difference of -$6410.80; 95% CI: -$9147.04 to -$3674.57; p<0.001) and the anterior-posterior approach (mean difference of -$14,685.62; 95% CI: -$19,331.61 to -$10,039.63; p<0.001). The intra-operative cost of the posterior approach was also significantly less than that of the anterior-posterior approach (mean difference of -$8274.82; 95% CI: -$12,762.62 to -$3787.01; p<0.001). This trend also held true for post-operative costs between anterior and posterior approaches (mean difference of -$4136.90; 95% CI: -$7256.64 to -$1017.15; p<0.05). These results can be visualized in Figures 2 and 3.

|

Figure 2 Total and Component Costs Across Surgery Types. |

|

Figure 3 Average Costs by Surgery Type and Phase of Care. |

Total episode costs for the anterior approach were significantly less than that of the posterior approach (mean difference of -$10,434.99; 95% CI: -$14,200.11 to -$6778.78, p<0.001) and anterior-posterior approach (mean difference of -$17,048.38; 95% CI: -$23,441.37 to -$10,655.39, p<0.001). Total episode costs for the posterior approach were significantly less than that of the anterior-posterior approach (mean difference of -$6613.39; 95% CI: -$12,788.71 to -$438.06; p<0.05).

When applying the same KW analysis to the components of pre-operative cost relative to the different surgery types, the only significant difference was a cheaper medical assistant (MA) cost for the anterior approach as compared to the posterior approach (mean difference of -$8.25; 95% CI: -$15.52 to -$0.99; p<0.05). Results of the same analysis of post-operative costs relative to different surgery types is shown in the Appendix.

Discussion

Experts predict that healthcare costs will represent a startling 20% of the United States’ gross domestic product within the next ten years.12 Overutilization of expensive services is suspected to be a major culprit, which has prompted interest in a shift from traditional “fee-for-service” models to various value-based payment models (VBPs). It is now estimated that at least 18% of healthcare dollars flow through some sort of VBP.13 The most commonly discussed VBP is a procedure-based bundled payment, wherein providers are paid a pre-determined sum for a ninety-day surgical episode. Such bundled payments have demonstrated only modest success in reducing costs, with one concern being that surgeons remain financially incentivized to maximize case volume and complexity.14,15 In response to this, there is now interest in moving upstream to condition-based bundled payments (CBP).16 In CBPs, providers are motivated to treat a diagnosis in the most cost-effective manner, whether that means no surgery or a less-invasive surgery. Surgeons are no longer incentivized to maximize their volume of costly and complex procedures; in fact, they could be penalized for doing so.

To understand how spine surgeons might be impacted by CBPs, we must be able to estimate and compare total episode costs between different surgical options that are appropriate for a given spinal diagnosis. Here we took a step in this direction by comparing “scheduling-to-discharge” costs for anterior, posterior, and anterior-posterior cervical fusions for cervical myelopathy using TDABC.

As expected, we found that more invasive surgeries (posterior and anterior-posterior fusions) were associated with higher total costs, after adjusting for confounders. This stemmed from increased intra-operative costs (more supplies, implants, and O.R. time) and post-operative costs (longer length of stay). Not surprisingly, pre-operative personnel costs did not differ among the different surgery types, as the tasks required to arrange those surgeries are similar. These findings are similar to results reported by Sethi et al for lumbar fusions.17

Our estimates for the actual dollar-value differences in total (scheduling-to-discharge) costs between the three surgery types may be relevant to practices preparing for CBPs. After adjusting for confounders, posterior cervical fusion was roughly $10,000 more costly than anterior fusion, and anterior-posterior fusion was roughly $17,000 more costly. We can only speculate as to what a CBP for cervical myelopathy might look like, but these differences are sizeable and could meaningfully influence surgeons’ practice patterns. Figure 4 visualizes this mindset shift – anterior-posterior cervical fusions are financially favorable for hospitals and surgeons in fee-for-service arrangements, but they could be the exact opposite with CBPs.

|

Figure 4 Schematic of Condition-Based Reimbursement for Cervical Myelopathy. |

It is important to note that, by virtue of employing TDABC, the costs we have studied here are from the perspective of the providers, not the payers (as is common in many health economics studies). This enables a granular analysis of cost drivers that would otherwise be challenging. For example, our regression models confirmed that implants and supplies helped explain differences in intra-operative costs, while utilization of personnel such as physical therapists and ICU physicians helped explain differences in post-operative costs. Although these findings are not surprising, they speak to the power of detailed process mapping as part of TDABC. By studying nearly every type of personnel cost from time of scheduling to post-operative discharge, one can identify modifiable elements of care pathways. Surgical practices can use this strategy to continually reduce waste and drive down costs while maintaining outcomes.

Limitations

One of the notable limitations to this study is its retrospective nature. Additionally, our preoperative and postoperative costs only include personnel cost, rather than a more comprehensive integration of the costs of both personnel and supplies. As previously stated, we are missing key overhead and administrative costs such as real estate fees, upkeep costs, labs and imaging ordered, and overall daily room cost. This likely leads to an underestimation of the cost of a longer hospital stay. In future studies, we hope to integrate all aspects of costing into our analysis. Nonetheless, in this study we demonstrate the importance of assigning cost to all personnel involved in an episode of care, rather than exclusively thinking of cost as a composite of charges and/or material resources such as implants. Another key limitation of our study is the relatively small sample size and the fact that the cost data are derived from a single, tertiary academic institution. Consequently, regional fee structures and practice patterns may limit the generalizability of our findings to other settings or geographic areas.

Similarly, our study also does not account for outcomes associated with these cases, including pain improvement, functional improvement, need for further operations, and the lost or gained opportunity cost of the patient’s life. This is a key component in the value equation and should be accounted for in these analyses. A final limitation of our study is that we do not assign cost to the entirety of the pre- and post-operative visits. We only account for the most final pre-operative visit, even though it is common for patients to see their surgeon multiple times in their work up. In a similar vein, we do not account for the post-operative follow up, instead only assigning cost to the time until discharge. Clearly, follow-up visits also entail costs to the hospital such as additional imaging or consultant referrals, and this period is not captured in our study. Going forward, our goal is to characterize all these steps to create a more comprehensive cost calculation. As such, we recommend caution when using these numbers to determine the exact cost to care for these patients. The value in these analyses is in demonstrating the framework and methodology by which to perform the cost calculations, and in the elucidation of cost drivers. Application of these methods will help healthcare professionals identify and eliminate waste, optimizing the value we are able to provide our patients.

Conclusion

We have demonstrated the feasibility of TDABC for estimating a large fraction of total episode costs for the surgical treatment of cervical myelopathy. This may also be the first attempt at understanding episode costs across multiple surgical options for a given spinal diagnosis, which will be relevant as condition-based bundled payments emerge. As expected, anterior cervical surgeries incurred lower costs than posterior surgeries, which incurred lower costs than anterior-posterior surgeries.

Funding

There is no funding to report.

Disclosure

Dr Srinivas Prasad reports personal fees from Stryker Spine, personal fees from DePuy Synthes, personal fees from MiRUS, grants from AO Spine, grants from NREF, outside the submitted work. Dr Joshua Heller reports personal fees from ATEC, personal fees from SI Bone, personal fees from Globus/Nuvasive, grants from Providence Medical Technology, personal fees from Surgalign, grants from Ethicon, personal fees from XTANT, personal fees from Highridge Medical, outside the submitted work. Dr Alexander Vaccaro reports personal fees from Globus, personal fees from Stryker, personal fees from Medtronic, personal fees from Atlas Spine, personal fees from Alphatec Spine, personal fees from SpineWave, personal fees from Spinal Elements, personal fees from Curiteva, personal fees from Elsevier, personal fees from Jaypee, personal fees from Stout Medical, personal fees from Taylor Francis/Hodder and Stoughton, personal fees from Wolters Kluwer, personal fees from Thieme, personal fees from Accelus, personal fees from Advanced Spinal Intellectual Properties, personal fees from Avaz Surgical, personal fees from AVKN Patient Driven Care, personal fees from Cytonics, personal fees from Deep Health, personal fees from Dimension Orthotics LLC, personal fees from Electrocore, personal fees from Flagship Surgical, personal fees from FlowPharma, personal fees from Rothman Institute and Related Properties, personal fees from Harvard Med Tech, personal fees from Innovative Surgical Design, personal fees from Jushi (Haywood), personal fees from Orthobullets, personal fees from Parvizi Surgical Innovation, personal fees from Progressive Spinal Technologies, personal fees from Sentryx, personal fees from Stout Medical, personal fees from See All AI, personal fees from ViewFi Health, personal fees from Medcura, personal fees from Ferring Pharmaceutical, personal fees from National Spine Health Foundation (NSHF), outside the submitted work; In addition, Dr Alexander Vaccaro has a patent SYSTEMS AND METHODS FOR CONTROLLING MULTIPLE SURGICAL VARIABLES issued to NuVasive Specialized Orthopedics, Inc., a patent Surgical implant and method of use issued to Warsaw Orthopedic, Inc., a patent SACRO-ILIAC JOINT IMPLANT SYSTEM AND METHOD issued to Warsaw Orthopedic, Inc., a patent Delivery systems, tools, and methods of use issued to Warsaw Orthopedic, Inc., a patent Spinal plate system for stabilizing a portion of a spine issued to Zimmer Spine, Inc., a patent DELIVERY SYSTEMS, DEVICES, TOOLS, AND METHODS OF USE issued to Osteotech, Inc., a patent Spinal implant issued to Warsaw Orthopedic, Inc., a patent Ratcheting fixation plate issued to Robert Farris, Jason May, Alexander Vaccaro, a patent Resorbable hollow devices for implantation and delivery of therapeutic agents issued to Susan Riley, Alexander Vaccaro, Joseph Tai. Dr Ahilan Sivaganesan reports royalties from Mirus, outside the submitted work. The authors report no to the conflicts of interest in this work.

References

1. Health spending. 2023.

2. Sharan AD, Schroeder GD, West ME, Vaccaro AR. Redesigning health care organizations: the influence of government policy and methods of payment. J Spinal Disord Tech. 2015;28(10):379–381. doi:10.1097/BSD.0000000000000336

3. Joynt Maddox KE, Orav EJ, Zheng J, Epstein AM. Year 1 of the bundled payments for care improvement-advanced model. N Engl J Med. 2021;385(7):618–627. doi:10.1056/NEJMsa2033678

4. Slotkin JR, Ross OA, Newman ED, et al. Episode-based payment and direct employer purchasing of healthcare services: recent bundled payment innovations and the Geisinger health system experience. Neurosurgery. 2017;80(4S):S50–S8. doi:10.1093/neuros/nyx004

5. Schroeder GD, Hilibrand AS, Kepler CK, et al. Utilization of time-driven activity-based costing to determine the true cost of a single or 2-level anterior cervical discectomy and fusion. Clin Spine Surg. 2018;31(10):452–456. doi:10.1097/BSD.0000000000000728

6. Ali DM, Leibold A, Harrop J, Sharan A, Vaccaro AR, Sivaganesan A. A multi-disciplinary review of time-driven activity-based costing: practical considerations for spine surgery. Global Spine J. 2023;13(3):823–839. doi:10.1177/21925682221121303

7. Sarikonda A, Leibold A, Ali DM, et al. What is the marginal intraoperative cost of using an exoscope or operative microscope for anterior cervical discectomy and fusion? A time-driven activity-based cost analysis. World Neurosurg. 2024;181:e3–e10. doi:10.1016/j.wneu.2023.11.069

8. Sarikonda A, Leibold A, Sami A, et al. Do Busier surgeons have lower intraoperative costs? An analysis of anterior cervical discectomy and fusion using time-driven activity-based costing. Clin Spine Surg. 2024;37:E455–E463. doi:10.1097/BSD.0000000000001628

9. Sarikonda A, Tecce E, Leibold A, et al. What is the marginal cost of using robot assistance or navigation for transforaminal lumbar interbody fusion? A time-driven activity-based cost analysis. Neurosurgery. 2024;95:556–565. doi:10.1227/neu.0000000000002899

10. Tecce E, Sarikonda A, Leibold A, et al. Does body mass index influence intraoperative costs and operative times for anterior cervical discectomy and fusion? A time-driven activity-based costing analysis. World Neurosurg. 2024;185:e563–e571. doi:10.1016/j.wneu.2024.02.074

11. Neifert SN, Martini ML, Yuk F, et al. Predicting trends in cervical spinal surgery in the United States from 2020 to 2040. World Neurosurg. 2020;141:e175–e81. doi:10.1016/j.wneu.2020.05.055

12. NHE fact sheet: centers for medicare & medicaid services. 2022.

13. Measuring progress: adoption of alternative payment models in commercial, Medicaid, medicare advantage, and traditional medicare programs: health care payment learning & action network. 2023.

14. Hussey PS, Mulcahy AW, Schnyer C, Schneider EC. Closing the quality gap: revisiting the state of the science (vol. 1: bundled payment: effects on health care spending and quality). Evid Rep Technol Assess. 2012;(208.1):1–155.

15. Weeks WB, Rauh SS, Wadsworth EB, Weinstein JN. The unintended consequences of bundled payments. Ann Intern Med. 2013;158(1):62–64. doi:10.7326/0003-4819-158-1-201301010-00012

16. Andrawis JP, McClellan M, Bozic KJ. Bundled payments are moving upstream. N Engl J Med Catal. 2019.

17. Sethi RK, Drolet CE, Pumpian RP, et al. Combining time-driven activity-based costing and lean methodology: an initial study of single-level lumbar fusion surgery to assess value-based healthcare in patients undergoing spine surgery. J Neurosurg Spine. 2022:1–7.

© 2025 The Author(s). This work is published and licensed by Dove Medical Press Limited. The

full terms of this license are available at https://www.dovepress.com/terms.php

and incorporate the Creative Commons Attribution

- Non Commercial (unported, 4.0) License.

By accessing the work you hereby accept the Terms. Non-commercial uses of the work are permitted

without any further permission from Dove Medical Press Limited, provided the work is properly

attributed. For permission for commercial use of this work, please see paragraphs 4.2 and 5 of our Terms.

© 2025 The Author(s). This work is published and licensed by Dove Medical Press Limited. The

full terms of this license are available at https://www.dovepress.com/terms.php

and incorporate the Creative Commons Attribution

- Non Commercial (unported, 4.0) License.

By accessing the work you hereby accept the Terms. Non-commercial uses of the work are permitted

without any further permission from Dove Medical Press Limited, provided the work is properly

attributed. For permission for commercial use of this work, please see paragraphs 4.2 and 5 of our Terms.